Advisor Valuation Report: What It Is, What It Includes, and How to Use It to Make Smarter Decisions

There’s a moment most financial advisors hit—sometimes quietly, sometimes with a jolt—when they realize their practice is more than a book of clients. It’s an asset. A business. A future exit. A legacy.

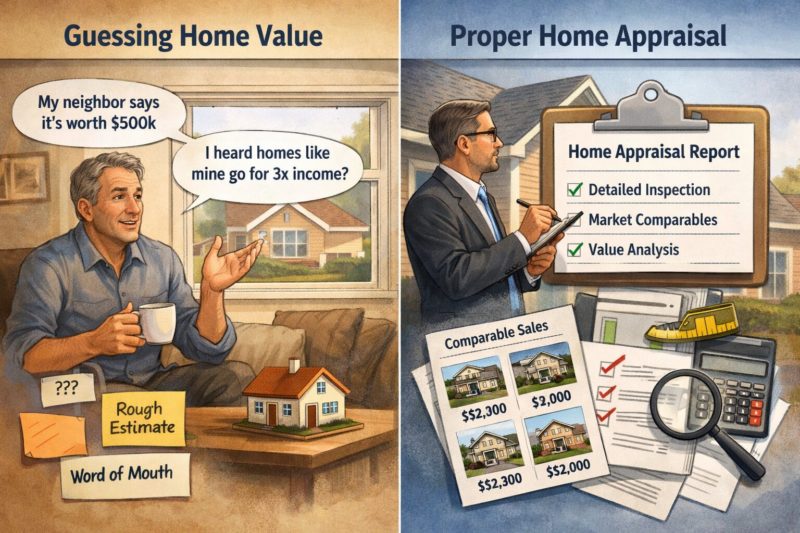

And yet, many advisors still rely on rough rules of thumb when they think about value: “I’ve heard it’s X times revenue,” or “My friend sold for Y.” That’s like pricing a house based on what your neighbor thinks it’s worth—without an inspection, comps, or a clear understanding of what drives the price up or down.

That’s exactly where an advisor valuation report comes in: a structured, evidence-based way to understand what your practice is worth today, what it could be worth in the future, and what you can do—practically—to increase that value.

This guide breaks down what an advisor valuation report typically includes, how it’s built, what data you should prepare, and how you can use the results for better decisions (whether you’re buying, selling, planning succession, or simply tightening up operations).

What Is an Advisor Valuation Report?

An advisor valuation report is a professional assessment of a financial advisory practice’s value—usually expressed as a fair market value range, with supporting analysis that explains:

- What your practice is worth (and why)

- Which factors increase or reduce value

- How your metrics compare to peers

- What levers you can pull to improve valuation

- How deal terms and taxes can affect the real money you keep

Think of it as both a valuation and a business health report. A solid one doesn’t just give you a number; it shows you the drivers behind the number.

Why a Valuation Report Matters More Than Ever

The advisory market has matured. Buyers are more sophisticated, capital is more active, and consolidation continues. That means:

- “Average multiples” aren’t enough.

Two firms can have the same revenue and wildly different valuations because of client demographics, revenue quality, growth rate, expense structure, and concentration risk. - Deal terms can change the true value.

A headline price might look great—until you realize half of it is an earnout that’s hard to achieve, or the tax treatment is unfavorable. - You may be undervaluing your own leverage.

If you know what your practice is worth (and what the market values), you negotiate differently. You plan differently. You invest differently. - Valuation is useful long before you sell.

Many advisors wait until they’re ready to exit. But the best time to understand your value is when you still have time to improve it.

When You Should Get an Advisor Valuation Report

You don’t need to be “one foot out the door” to benefit. A valuation report is especially useful when:

- You’re considering succession planning or an internal transition

- You want to sell (now or within the next 1–5 years)

- You’re evaluating a merge or acquisition

- You’re bringing on a partner or restructuring equity

- You’re planning your retirement timeline

- You want a clearer sense of how your growth strategy affects enterprise value

- You need support for strategic planning or lender conversations

What a Strong Advisor Valuation Report Typically Includes

Not all valuation reports are created equal. But the best ones share a similar structure and focus on three things:

- The value conclusion

- The proof behind it

- Practical recommendations to move the number

Here are the core components you should expect.

Fair Market Value (and What It Actually Means)

Most professional valuations aim to estimate fair market value—the price at which a willing buyer and seller would transact, with neither forced and both having reasonable knowledge of the facts.

A good report clarifies:

- What’s included (e.g., operating assets, goodwill)

- What’s excluded (e.g., non-operating assets, cash, real estate, unusual liabilities)

- The valuation date and the “premise” (going concern vs. liquidation)

This matters because “value” changes depending on assumptions—and you want your valuation to align with your real-world situation.

Peer-Based Benchmarking (How You Stack Up)

One of the most useful elements of modern advisor valuation reporting is peer comparison. This is where the report goes beyond “times revenue” and starts answering more valuable questions:

- Is your expense structure efficient compared to similar practices?

- Do you have healthy new client flow—or are you coasting on existing relationships?

- Are you overly dependent on a small number of high-value households?

- Are your clients aging faster than you’re replacing them?

Benchmarking typically looks at data like:

- AUM

- Revenue and revenue mix (recurring vs. transactional)

- Expenses and profitability

- Client counts and growth

- Net flows

- Advisor tenure and retirement horizon

Key Value Drivers and Value Detractors

This is the section buyers care about most—because it speaks directly to risk and scalability.

Common value drivers include:

- High recurring revenue (predictable, sticky)

- Strong organic growth and net inflows

- Diversified client base (low concentration risk)

- Younger client demographics (longer lifetime value)

- Documented processes and scalable operations

- A team structure that reduces key-person dependency

Common detractors:

- Heavy reliance on one rainmaker advisor

- High client concentration (too much revenue tied to too few households)

- Aging client base with weak acquisition engine

- Low profitability due to bloated overhead

- Weak succession plan / unclear continuity

A report that spells these out clearly gives you a roadmap.

Profitability and Efficiency Analysis

Valuation isn’t just about top-line revenue—it’s about what revenue turns into.

Many reports include:

- Margin analysis

- Expense categorization (fixed vs. variable)

- Efficiency indicators such as revenue per client, revenue per employee, cost-to-serve estimates

Even modest improvements here can materially impact valuation because buyers often model long-term cash flow.

Value Trajectory: Where Your Practice Is Headed

One of the most compelling ideas in valuation reporting is that value isn’t static. Some reports include a predictive view—how your valuation might evolve based on your current performance and trends.

This helps answer:

- If you change nothing, what happens to value in 3–5 years?

- What if you improve retention, profitability, or client acquisition?

- What if you shift your client mix younger?

This turns valuation into a planning tool, not just a number for a file folder.

Deal Terms and Tax Treatment (The “Real Money” Section)

The price is only part of the story. A strong report often provides clarity around:

- Deal structures (cash, seller notes, earnouts, equity rollovers)

- How common terms impact risk and expected payout

- Tax considerations (structure-dependent implications that affect net proceeds)

This is where many advisors get surprised. A slightly lower headline price with cleaner terms can outperform a “higher” offer with heavy contingencies.

The Data You’ll Typically Need to Provide

Most valuation report processes follow a structured intake where you submit practice metrics. You can expect to gather items like:

- Total revenue and recurring revenue

- AUM and recent inflows/outflows

- Number of active clients

- Expense totals and breakdowns

- New clients acquired in the last year

- Years in business and expected retirement horizon

- Client age distribution

- Historical revenue (often multiple years)

If you want your valuation to be accurate, the key is consistency and clarity. Clean inputs = credible outputs.

How to Prepare Before You Order a Valuation Report

If you want the report to be more than a “ballpark estimate,” do a little prep work first. It pays off.

Gather Clean Financials (and Separate Business vs. Personal)

Many advisory practices have “mixed” expenses (travel, meals, vehicles). A valuation can adjust for discretionary items, but only if you document them clearly.

Know Your Revenue Quality

Break down recurring, transactional, planning, insurance/annuity-related revenue. Many valuation providers have specific scope rules depending on how the practice earns.

Identify Concentration Risk Early

Create a quick snapshot:

- Top 10 clients as a % of revenue

- Top 20 as a % of revenue

If you’re concentrated, it doesn’t mean your practice is “bad.” It means a buyer sees risk—and will price accordingly.

Pull Client Demographics

Even a simple age-band breakdown can add meaningful context to your valuation, because it affects expected retention and future cash flow.

How to Use Your Valuation Report (Beyond “Knowing the Number”)

Here’s where most advisors miss the point. The value conclusion is useful—but the strategy inside the report is what can change your outcome.

Use It as a Negotiation Tool

When you have a documented valuation, you’re no longer negotiating from emotion or hearsay. You have:

- Market-based support

- Benchmarked insights

- Specific drivers to discuss

Use It to Prioritize Growth Initiatives

A valuation report often clarifies which activities actually increase enterprise value. For example:

- Improving client acquisition channels

- Increasing recurring revenue percentage

- Streamlining operations and margins

- Reducing key-person dependency via team structure

Use It to Build a Smarter Succession Plan

If you’re transitioning internally, valuation clarity reduces friction and resentment. It creates a shared reference point for:

- Equity splits

- Buy-in/buy-out planning

- Timelines and milestones

Use It to Decide When to Sell

Sometimes the valuation reveals something simple:

- “You can sell now… but you’re leaving money on the table.”

- Or: “Your value is strong today; waiting may introduce risks (aging clients, slowing growth).”

Either outcome is useful—because it replaces guesswork with insight.

What to Look for in a Valuation Provider

If you’re choosing a provider, look for a process that’s:

- Clear and structured (no endless back-and-forth)

- Fast enough to be actionable (weeks, not months, unless the scope is complex)

- Transparent about what the report includes

- Able to explain the result in plain English (ideally with a review call)

- Grounded in industry benchmarks and real transaction context

Most importantly: choose a provider whose report gives you decision-grade clarity, not just a number.

Common Mistakes Advisors Make With Valuations

Only Focusing on the Multiple

Multiples are shorthand. The real story is the risk and durability of cash flow.

Getting a Valuation Too Late

If you’re 6 months from retirement and your valuation shows major detractors, you have limited time to fix them. Earlier is better.

Ignoring Deal Structure and Tax Implications

A “great number” can shrink quickly once you factor in terms, earnouts, and taxes.

Treating Valuation as a One-Time Event

The smartest firms treat valuation like a KPI—checked regularly and used to guide strategy.

A Simple Mindset Shift: “Valuation” Is a Growth Tool

The biggest takeaway is this:

An advisor valuation report isn’t only about selling.

It’s about building a more valuable business—whether you exit in 2 years or 12.

When you understand what the market rewards, you stop guessing. You start building with intention. And the irony is: the practices that plan best for a future sale are often the ones that become more enjoyable to run today—because they’re more organized, profitable, and resilient.

If you’re curious about your current value—or you want a clearer roadmap for increasing it—getting a valuation report can be one of the most practical steps you take this year.

Would you like to receive similar articles by email?

Paul Tomaszewski

Paul Tomaszewski is a science & tech writer as well as a programmer and entrepreneur. He is the founder and editor-in-chief of CosmoBC. He has a degree in computer science from John Abbott College, a bachelor's degree in technology from the Memorial University of Newfoundland, and completed some business and economics classes at Concordia University in Montreal. While in college he was the vice-president of the Astronomy Club. In his spare time he is an amateur astronomer and enjoys reading or watching science-fiction. You can follow him on LinkedIn and Twitter.

You May Also Like

4 Employee Benefits Every Trucker Should Have

4 Common Press Brake Applications in Manufacturing